Stablecoins are reconstructing traditional payments, from the issuance boom to integration victory

Jan 08, 2026 17:16:12

Written by: Mario Stefanidis

Compiled and organized by: BitpushNews

Stablecoins are undeniably making their way into traditional finance in a patchy yet significant manner.

Klarna has just launched KlarnaUSD on Stripe's first-layer network Tempo, built specifically for payments; PayPal's PYUSD, issued on Ethereum, has doubled in market capitalization within three months, surpassing 1% of the stablecoin market share, with supply nearing $4 billion; Stripe has now begun using USDC to pay merchants; Cash App has expanded its services from Bitcoin to stablecoins by early 2026, allowing its 58 million users to seamlessly send and receive stablecoins within their fiat balances.

Although each company approaches from different angles, they are all responding to the same trend: stablecoins make the flow of funds incredibly simple.

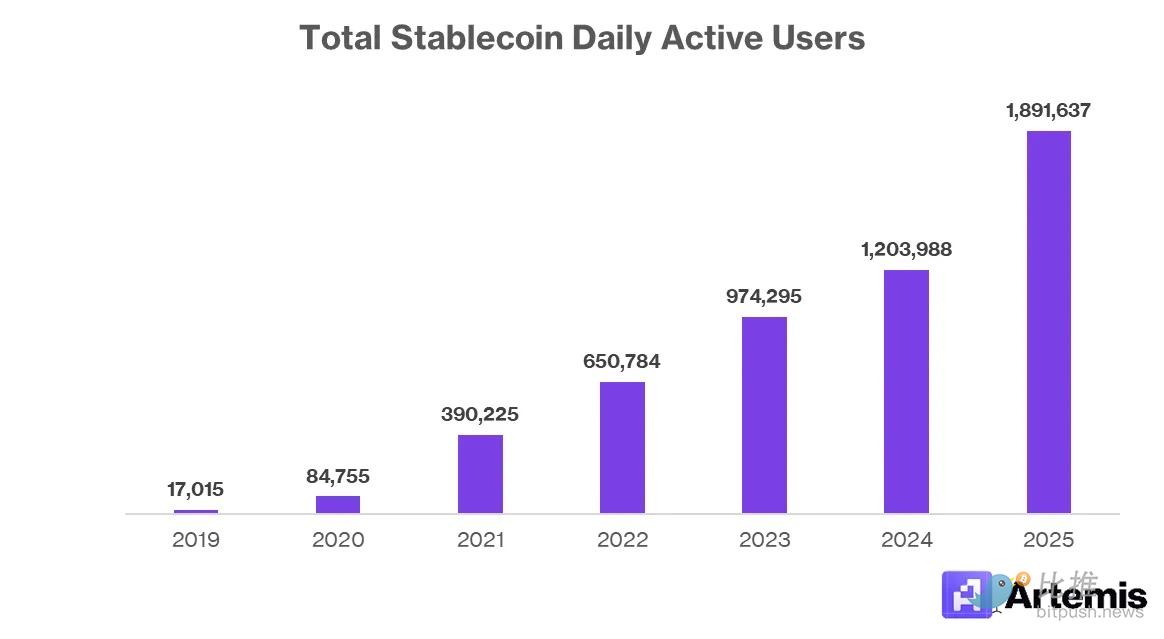

Data source: Artemis Analytics

Market narratives often jump straight to "everyone will issue their own stablecoin." But this outcome is not reasonable. A world with dozens of widely used stablecoins is manageable, but if there are thousands, it will descend into chaos. Users do not want their dollars (yes, dollars, which dominate over 99%) scattered across a long tail of branded tokens, each on its own chain, with different liquidity, fees, and exchange paths. Market makers earn spreads, cross-chain bridges charge fees—this layered "cutting in" is precisely the problem stablecoins aim to solve.

Fortune 500 companies should recognize that stablecoins are extremely useful, but issuing a stablecoin is not a guaranteed win. A select few companies will be able to leverage this to gain distribution channels, reduce costs, and strengthen their ecosystems. Meanwhile, many other companies may bear operational burdens without clear returns.

The real competitive advantage comes from how to embed stablecoins as "payment rails" into products, rather than just slapping their brand on a token.

Why Stablecoins Are Favored in Traditional Finance

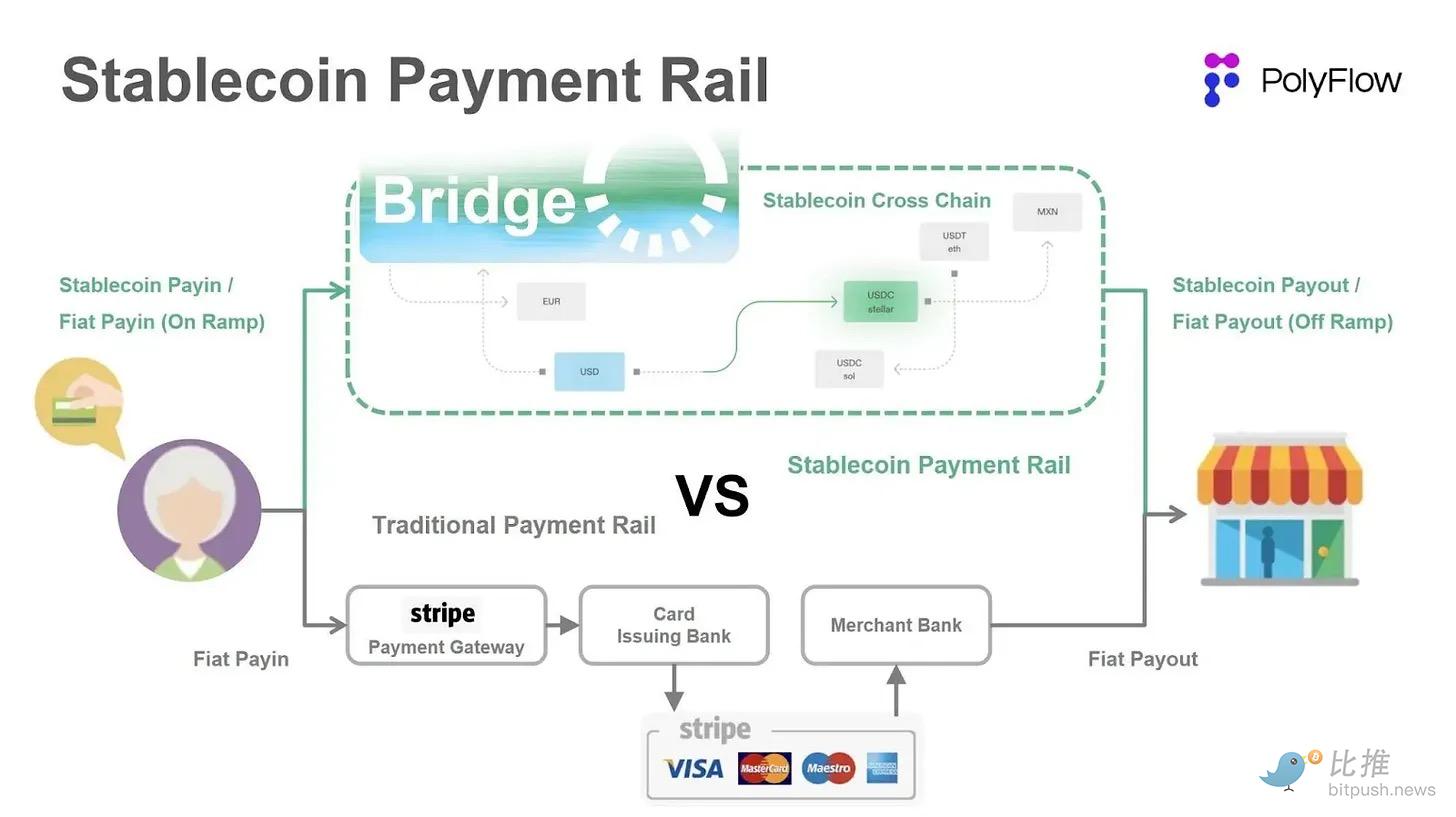

Stablecoins solve specific operational issues that legacy payment rails have failed to address for traditional companies. These benefits are easy to understand: lower settlement costs, faster fund availability, broader cross-border coverage, and fewer intermediaries. When a platform processes millions of transactions daily, with annual transaction volumes (TPV) reaching billions or even trillions of dollars, minor improvements can compound into significant economic benefits.

1. Lower Settlement Costs

Most consumer platforms accept card payments and pay interchange fees for each transaction. In the U.S., these fees can account for about 1%-3% of the transaction amount, plus a fixed transaction fee of about $0.10-$0.60 from the three major card networks (American Express, Visa, Mastercard). If payments remain on-chain, stablecoin settlements can reduce these fees to just a few cents. This is an attractive leverage point for companies with high transaction volumes and low margins. Note that they do not need to completely replace card payments with stablecoins; covering just a portion of the transaction volume can achieve cost savings.

Data source: A16z Crypto

Some companies choose to partner with service providers like Stripe to accept stablecoin payments settled in dollars. While this is not a necessary step, most businesses prefer zero volatility and instant fiat availability. Merchants typically want dollars to enter their bank accounts, rather than managing crypto custody, private keys, or dealing with reconciliation issues. Even the 1.5% floating fee charged by Stripe is significantly lower than credit card alternatives.

It is conceivable that large enterprises may initially collaborate with stablecoin processing solutions before weighing whether to invest in capital expenditures to build fixed infrastructure. Ultimately, this trade-off will also become reasonable for small and medium-sized enterprises that wish to retain nearly all the economic benefits.

2. Global Reach

Stablecoins can flow across borders without the need to negotiate with banks in each country. This advantage is appealing for consumer applications, marketplace platforms, gig platforms, and remittance products. Stablecoins enable them to reach users in markets that have yet to establish financial relationships.

End-user foreign exchange (FX) fees for credit cards typically add an extra 1%-3% per transaction, unless using cards that do not charge such fees. Stablecoins do not incur cross-border fees because their payment layer does not recognize national borders; sending USDC from a New York wallet to Europe is the same as sending locally.

For European merchants, the only additional step is deciding how to handle the received dollar-denominated assets. If they want their bank accounts to receive euros, they must exchange them. If they are willing to hold dollars on their balance sheets, no exchange is necessary, and they may even earn returns if they leave the balance idle on exchanges like Coinbase.

3. Instant Settlement

Stablecoins settle in minutes, often in seconds, while traditional payment transfers may take days. Moreover, the former operates 24/7, unaffected by bank holidays, cut-off times, and other inherent barriers of traditional banking systems. Stablecoins eliminate these constraints, significantly reducing operational friction for companies managing high-frequency payments or tight working capital cycles.

How Traditional Companies Should Approach Stablecoins

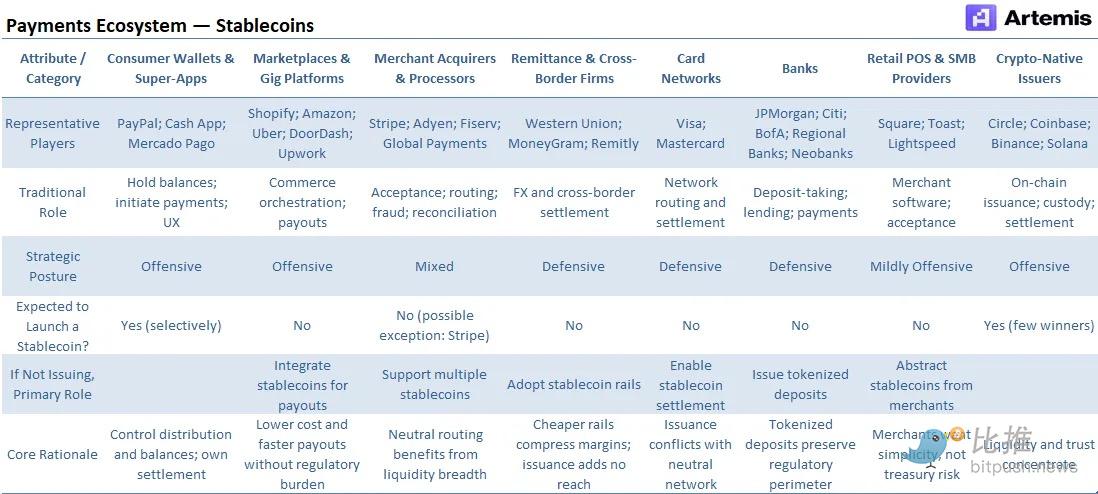

Stablecoins create both opportunities and pressures. Some companies can leverage them to expand product coverage or reduce costs, while others may face the risk of losing some economic benefits if users shift to cheaper or faster rails. The right strategy depends on the company's revenue model, geographic distribution, and its reliance on legacy payment infrastructure.

Some companies benefit from adding stablecoin rails because it strengthens their core products. Platforms already serving cross-border users can settle funds faster and avoid the friction of establishing relationships with local banks. If they handle millions of transactions, they can lower settlement costs when payments remain on-chain.

Many large platforms operate on thin transaction profit margins. If stablecoins allow platforms to bypass even 1-3 basis points of costs on some fund flows, the savings can be substantial. At an annual transaction volume of $1 trillion, reducing costs by 1 basis point is worth $100 million. Companies taking an aggressive stance include fintech-native, capital-light payment rails like PayPal, Stripe, and Cash App.

Other companies adopt stablecoins because competitors may use them to bypass parts of their business model. For example, banks and custodians face significant risks from stablecoins, as they may siphon off market share from traditional deposits, leading to a loss of low-cost funding sources. Issuing tokenized deposits or providing custody services may offer them an early line of defense against new entrants.

Stablecoins also lower the cost of cross-border remittances, which means remittance businesses face risks. Defensive adoption is more about preventing existing revenue from being eroded rather than growth. Companies in the defensive camp vary widely, from Visa and Mastercard, which charge interchange fees and provide settlement services, to Western Union and MoneyGram on the remittance front, as well as banks of various sizes that rely on low-cost deposits.

Given that slow adoption of stablecoins in the payment space, whether on the offensive or defensive, could pose a survival threat, the question for Fortune 500 companies shifts to: is it more meaningful to issue their own stablecoin or integrate existing tokens?

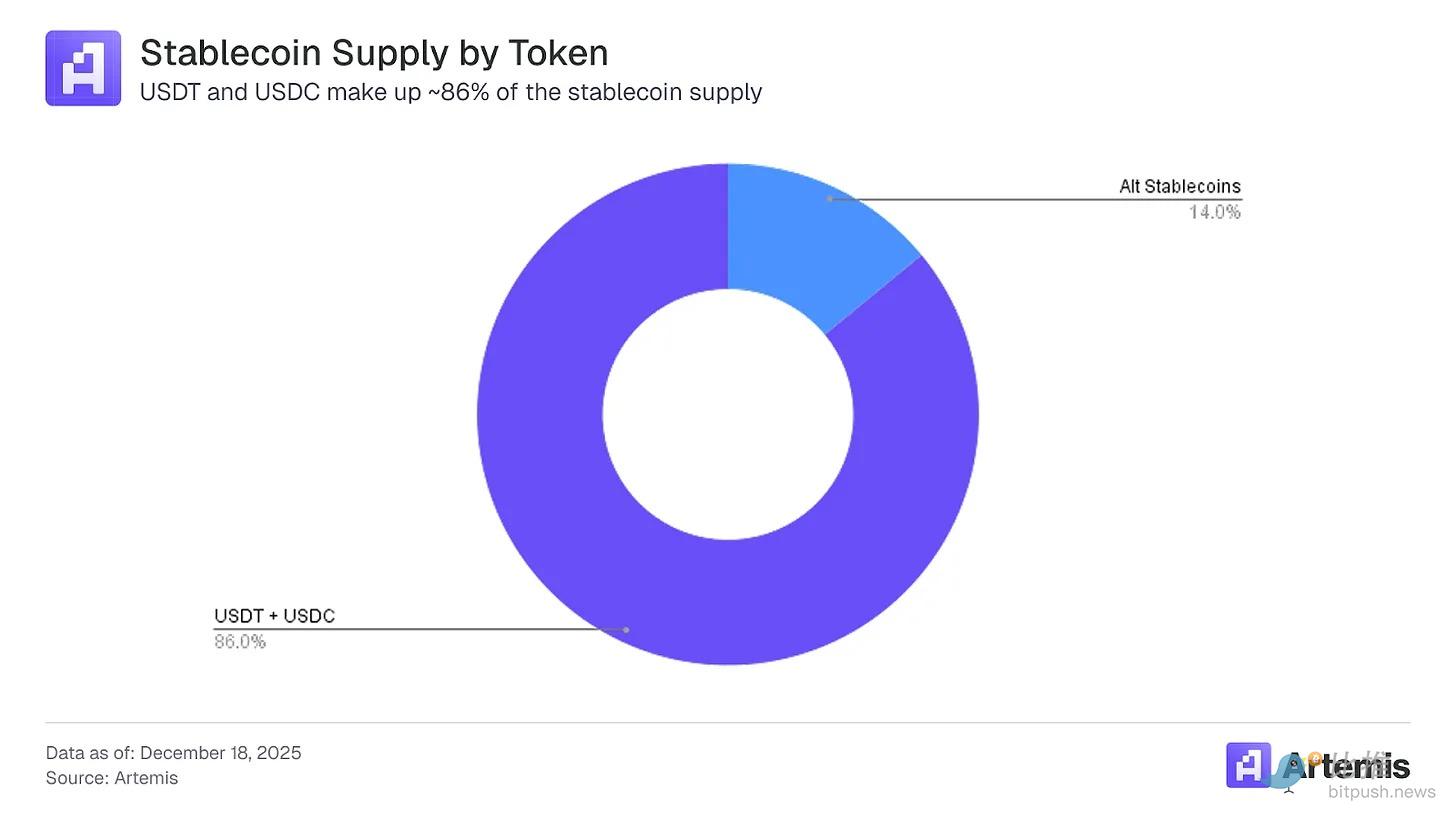

Data source: Artemis Analytics

It is not a sustainable equilibrium for every company to issue stablecoins. Users want their stablecoin experience to be frictionless, and if they have to sift through dozens of branded tokens in their wallets, even if they are all denominated in the same currency, they may prefer fiat.

Supply Trajectory

Companies should assume that only a small number of stablecoins can maintain deep liquidity and broad acceptance. However, this is not a "winner-takes-all" industry. For example, Tether's USDT was the first fiat-backed stablecoin, debuting in October 2014 on Bitcoin's Omni Layer. Despite competitors emerging, including Circle's USDC launched in 2018, its dominance in stablecoins peaked in early 2024, exceeding 71%.

As of December 2025, USDT's dominance in total stablecoin supply is 60%, with USDC in second place at 26%. This means that other alternatives control about 14% of the total pool of approximately $310 billion (around $43 billion). While this may not sound like much compared to the trillions of dollars in equity or fixed income markets, the total supply of stablecoins has grown 11.5 times from $26.9 billion in January 2021, with a compound annual growth rate of 63% over the past five years.

Even with a more moderate annual growth rate of 40%, by 2030, the supply of stablecoins could reach approximately $1.6 trillion, more than five times its current value. The year 2025 will be crucial for the sector, thanks to significant regulatory clarity brought by the GENIUS Act and large-scale institutional adoption driven by clear use cases.

By then, the combined dominance of USDT and USDC may also decline. At the current rate of decline of 50 basis points per quarter, by 2030, other stablecoins could occupy 25% of the market, based on our supply forecast of around $400 billion. This is a considerable figure, but clearly insufficient to support dozens of tokens the size of Tether or USDC.

When there is a clear product-market fit, adoption can happen rapidly, benefiting from the tailwinds of broader stablecoin supply growth while potentially capturing market share from existing leaders. Otherwise, newly issued stablecoins may get lost in the "mishmash" of low-supply, unclear growth story stablecoins.

Note that among the 90 stablecoins currently tracked by Artemis, only 10 have a supply exceeding $1 billion.

Case Studies of Enterprises

Companies experimenting with stablecoins do not follow a single script. Each company is responding to its own business pain points, and these differences are often more significant than their similarities.

PayPal: Defending Core Business While Testing New Rails

PYUSD is primarily a defensive product, and only secondarily a growth product. PayPal's core business still operates on card and bank transfer transactions, which is also the source of most of its revenue. The rates for branded checkouts and cross-border transactions are significantly higher.

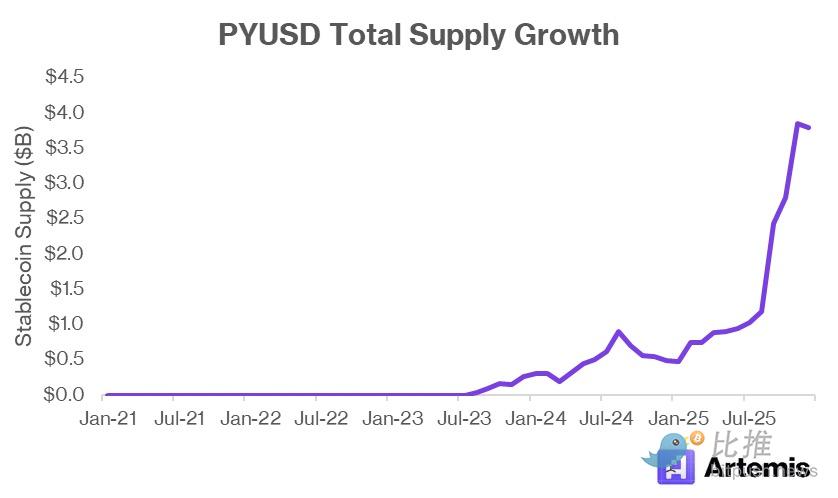

Stablecoins threaten this stack by offering cheaper settlements and faster cross-border flows. PYUSD allows PayPal to participate in this shift while maintaining control over user relationships. As of the third quarter of 2025, the company reported having 438 million active accounts—defined as users who have transacted on the platform in the past 12 months.

PayPal already holds user balances, manages compliance, and operates a closed-loop ecosystem. Issuing a stablecoin naturally aligns with this structure. The challenge lies in adoption, as PYUSD competes with USDC and USDT, which already have deeper liquidity and broader acceptance. PayPal's advantage lies in distribution, not price. PYUSD is only effective if PayPal can embed it into the workflows of PayPal and Venmo.

Data source: Artemis Analytics

PYUSD is similar to Venmo, both being growth vehicles for PayPal but not direct revenue generators. In 2025, Venmo is expected to generate about $1.7 billion in revenue, accounting for only about 5% of its parent company's total revenue. However, the company is successfully monetizing through the Venmo debit card and "Pay with Venmo" product.

Currently, PYUSD offers users a 3.7% annualized reward rate for holding the stablecoin in their PayPal or Venmo wallets, meaning PayPal is at best breaking even from a net interest margin perspective (holding U.S. Treasury bonds as collateral for the supply). The real opportunity comes from fund flows, not idle funds. If PYUSD reduces PayPal's reliance on external rails, lowers settlement costs for certain transactions, and keeps users within the ecosystem rather than flowing out to other platforms, PayPal will be a net beneficiary.

Additionally, PYUSD supports a defensive economy. The "disintermediation" of open stablecoins like USDC is a real risk, and by providing its own stablecoin, PayPal reduces the likelihood that its services become something users must pay for or bypass.

Klarna: Reducing Payment Friction

Klarna's focus on stablecoins is on control and cost. As a "buy now, pay later" provider, Klarna sits between merchants, consumers, and card networks. It pays interchange and processing fees on both ends of the transaction. Stablecoins provide a way to compress these costs and simplify settlements.

Klarna helps consumers finance purchases in the short and long term. For payment plans over a few months, Klarna typically charges 3-6% per transaction plus about $0.30. This is the company's largest source of revenue, compensating for its processing of payments, assuming credit risk, and increasing merchant sales. Klarna also offers longer installment plans (such as 6, 12, or 24 months), with interest rates similar to credit cards.

In both cases, Klarna's focus is not on becoming a payment network but on managing internal cash flows. If Klarna can settle with merchants faster and cheaper, it can improve margins and strengthen merchant relationships.

The risk lies in fragmentation—unless Klarna-branded tokens are widely accepted outside its platform, holding token balances long-term does not benefit Klarna. In short, for Klarna, stablecoins are a tool, not a product.

Stripe: Being the Settlement Layer, Not Issuing Tokens

Stripe's approach can be described as the most disciplined. It chooses not to issue stablecoins but focuses on using existing stablecoins for payments and collections. This distinction is important because Stripe does not need to win liquidity; it needs to win fund flows.

Stripe's annual transaction volume is expected to grow by 38% year-on-year in 2024, reaching $14 trillion; at this rate, despite being established over a decade later, the platform could surpass PayPal's $18 trillion in annual transaction volume. The company's recently reported valuation of $106.7 billion reflects this growth.

The company's support for stablecoin payments reflects clear customer demand. Merchants want faster settlements, fewer banking restrictions, and global coverage. Stablecoins address these issues. By supporting assets like USDC, Stripe improves its product without requiring merchants to manage another balance or bear issuer risk.

Earlier this year, the acquisition of Bridge Network for $1.1 billion solidified this strategy. Bridge focuses on stablecoin-native payment infrastructure, including deposit and withdrawal channels, compliance tools, and global settlement rails. Stripe's acquisition of Bridge was not to issue tokens—but to internalize the pipeline. This move gives Stripe more control over its stablecoin strategy and improves the integration of existing merchant workflows.

Data source: PolyFlow

Stripe wins by becoming the interface for stablecoins. Its strategy reflects its market position, processing trillions of dollars in transaction volume while maintaining double-digit annual growth rates. Regardless of which token dominates, Stripe remains neutral and charges fees based on transaction volume. Given the extremely low costs of underlying stablecoin transactions, any fixed fees Stripe can charge in this new market will bolster its profits.

Merchant Pain Points: Simplicity is Justice

The reason merchants are interested in stablecoins is simple: high costs of accepting payments, and these costs are evident.

In 2024, U.S. merchants paid $18.72 billion in processing fees to accept $11.9 trillion in customer payments. For many small and medium-sized enterprises, these fees are the third-largest operational expense after labor and rent. Stablecoins provide a viable way to alleviate this burden in specific use cases.

In addition to lower fees, stablecoins also offer predictable settlements and faster fund availability. On-chain transactions provide finality, while credit cards or traditional payment processing solutions may encounter refunds or disputes. Merchants also do not want to hold cryptocurrencies or manage wallets, which is why early pilots look like "stablecoins in, dollars out."

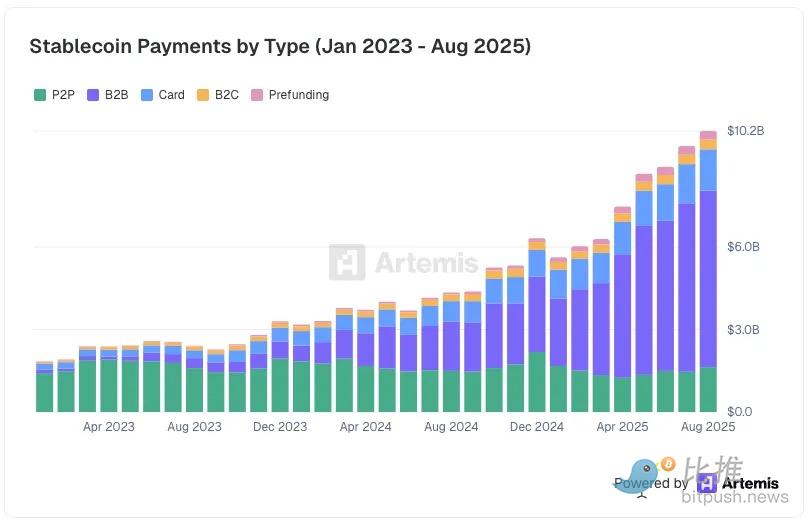

According to a recent survey conducted by Artemis in August 2025, merchants are already processing $6.4 billion in business-to-business stablecoin payments, ten times the volume processed in December 2023.

Data source: Artemis Analytics

This dynamic also explains why merchant adoption tends to concentrate rapidly. Merchants do not want to support dozens of tokens, each with different liquidity conditions, conversion costs, and operational characteristics. Each additional stablecoin introduces complexity and reconciliation challenges from market makers or cross-chain bridges, undermining the initial value proposition.

Thus, merchant adoption favors stablecoins with clear product-market fit. Stablecoins lacking characteristics that make transactions easier than fiat will gradually disappear. From a merchant's perspective, accepting a long-tail stablecoin does not offer significant advantages compared to not accepting any stablecoin at all.

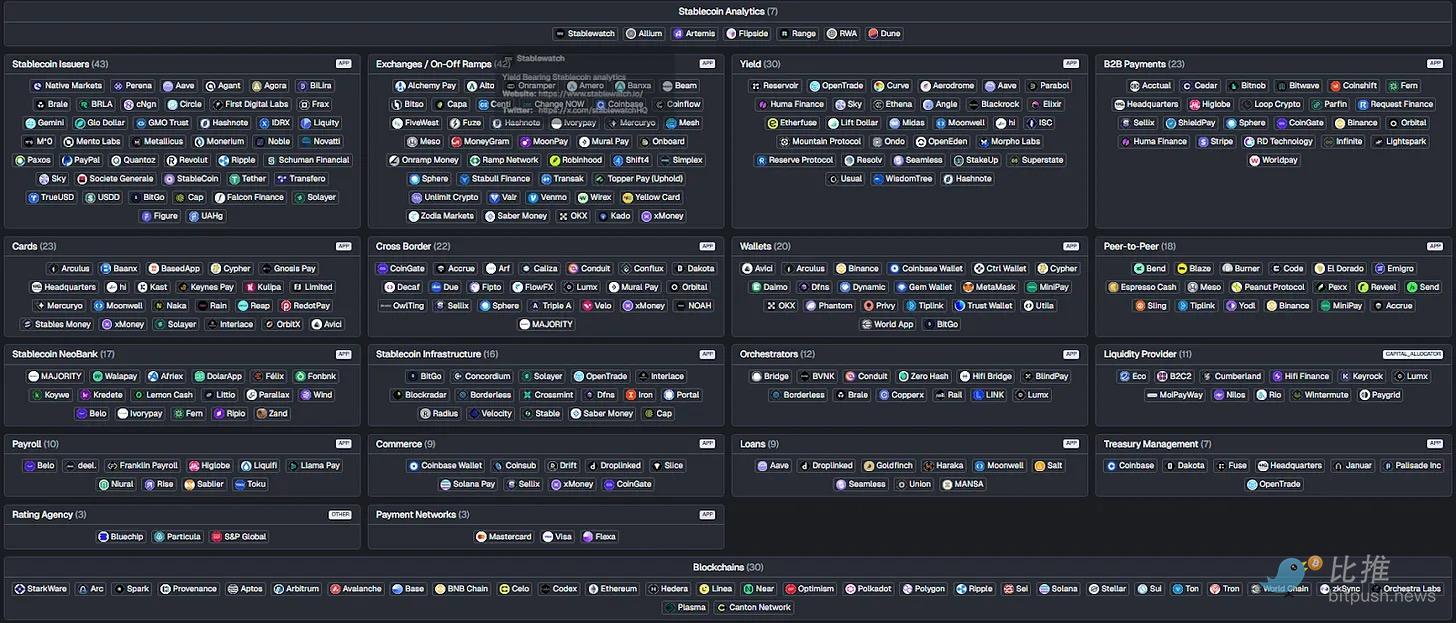

The Artemis stablecoin map illustrates how chaotic the current landscape is. Merchants will not deal with dozens of deposit and withdrawal channels, wallets, and infrastructure providers just to convert revenue into fiat.

Data source: Artemis (stablecoinsmap.com)

Data source: Artemis (stablecoinsmap.com)

Merchants reinforce this outcome by standardizing the use of effective solutions. Processors reinforce this outcome by only supporting assets that customers actually use. Over time, the ecosystem will aggregate around a limited number of tokens that are worth the integration costs.

Why This Matters

The implications of all this are unsettling for a large part of the stablecoin ecosystem: simply "issuing" is not a sustainable business model.

A company whose main product is "we mint stablecoins" is betting that liquidity, distribution, and usage will naturally arise. In reality, these things only emerge when a token is embedded in real payment flows. The idea that "if you mint it, they will come" does not apply here, as consumers face choices from hundreds of issuers.

This is why companies like Agora or M0, which only focus on issuance, will struggle to explain their long-term advantages unless they significantly expand their business beyond minting. If they cannot control wallets, merchants, platforms, or settlement rails, they are downstream from the value they are trying to capture. If users can just as easily hold USDC or USDT, there is no reason for liquidity to disperse into another branded dollar token.

In contrast, companies that control distribution, fund flows, or integration points will become stronger. Stripe can benefit without issuing stablecoins; it is directly on the path of merchant settlements and can earn revenue regardless of which token dominates. PayPal can justify PYUSD because it has wallets, user relationships, and checkout experiences. Cash App can integrate stablecoins because it has already aggregated balances and controls the user experience. These companies gain leverage from usage.

The real insight is that if you are upstream in the stack but only have a bare token, you are in a market destined for high consolidation.

Stablecoins reward your position in the architecture, not novelty.

Conclusion

Stablecoins change the way money flows, not the essence of money itself. Their value comes from reducing settlement friction, not creating new financial instruments. This fundamental distinction explains why the adoption of stablecoins occurs within existing platforms rather than parallel to them. Enterprises leverage stablecoins to optimize existing business processes, not to disrupt their business models.

This also explains why issuing stablecoins should not be the default choice. Liquidity, acceptance, and integration capabilities are far more important than branding. Without sustained use cases and clear demand, new tokens will only add operational burdens rather than create advantages. For most enterprises, integrating existing stablecoins is more scalable than issuing their own—markets naturally favor a few assets that can be universally applied rather than a multitude of tokens that only fit narrow scenarios. Before minting a doomed stablecoin, its offensive or defensive strategic positioning must be clear.

Merchant behavior further reinforces this trend. Merchants always seek simplicity and reliability. They will only adopt payment methods that reduce costs without adding complexity. Stablecoins that can seamlessly integrate into existing workflows will be favored; those requiring additional reconciliation, conversion steps, or wallet management will be eliminated. Over time, the ecosystem will filter down to a few stablecoins with clear product-market fit.

In the payment space, simplicity determines adoption, and only stablecoins that make the flow of funds easier will survive; the rest will ultimately be forgotten.

Latest News

ChainCatcher

Jan 16, 2026 13:58:54

ChainCatcher

Jan 16, 2026 13:57:48

ChainCatcher

Jan 16, 2026 13:52:54

ChainCatcher

Jan 16, 2026 13:50:46

ChainCatcher

Jan 16, 2026 13:39:49